All Our Stories

TOPICS

Agriculture & Animals

Arts & Culture

Books

Bug Bites

Film & TV

Food & Drink

History

Music

Sounds of Texas

Heel To Toe

Sports

Stories From Texas

Texan Translation

Typewriter Rodeo

Weekend Trip Tips

Where There’s Smoke

Border & Immigration

Business & Economy

Crime & Justice

Disability in Texas

Education

Energy & Environment

Government & Politics

Child Welfare

PolitiFact Texas

Week in Texas Politics

Health & Science

Housing

Military and Veterans’ Affairs

Partner Organizations

The Texas Newsroom

Race & Identity

Tech & Innovation

Transportation

FIND A SHOW

Podcasts

Texas Standard

Stories from Texas

Typewriter Rodeo

Recent Shows

Specials

Show Archives

About Us

About Us

How to Listen

Contact Us

Newsletters

The Talk of Texas

FAQ

All Our Stories

TOPICS

Agriculture & Animals

Arts & Culture

Books

Bug Bites

Film & TV

Food & Drink

History

Music

Sounds of Texas

Heel To Toe

Sports

Stories From Texas

Texan Translation

Typewriter Rodeo

Weekend Trip Tips

Where There’s Smoke

Border & Immigration

Business & Economy

Crime & Justice

Disability in Texas

Education

Energy & Environment

Government & Politics

Child Welfare

PolitiFact Texas

Week in Texas Politics

Health & Science

Housing

Military and Veterans’ Affairs

Partner Organizations

The Texas Newsroom

Race & Identity

Tech & Innovation

Transportation

FIND A SHOW

Podcasts

Texas Standard

Stories from Texas

Typewriter Rodeo

Recent Shows

Specials

Show Archives

About Us

About Us

How to Listen

Contact Us

Newsletters

The Talk of Texas

FAQ

Business & Your Money

July 1, 2026

Trump says the US doesn’t need a trade deal with its neighbors. Farm groups push hard for renewal

0

June 30, 2026

For beef prices to drop, ranchers need to raise more cattle. Here’s why they’re not

0

June 29, 2026

Here’s what borrowers need to know ahead of July 1 student loan changes

0

June 25, 2026

Report looks at rise of ‘junk fees’ renters face at apartments managed by Greystar

0

June 11, 2026

FIFA says the World Cup will be big for the North Texas economy. Experts aren’t so sure

0

June 9, 2026

Texas rule targeting smokable hemp is back in effect

0

May 13, 2026

Companies moving their legal homes to Texas is good PR, but don’t expect many new jobs

0

May 12, 2026

Adult education helps people make more money. Could it be a solution to rising costs?

0

May 4, 2026

Alex Jones’ Infowars site has finally shut down — for now

0

May 1, 2026

Court order allows smokable hemp to stay on shelves in Texas

0

May 1, 2026

Texas delta-8 ban may have hurt hemp businesses — but enforcement freeze must end, justices say

0

May 1, 2026

Classroom in a kitchen: How a Dallas cafe connects people with disabilities to hands-on job training

0

May 1, 2026

The Onion’s acquisition of Austin-based Infowars is on hold — for now

0

April 30, 2026

FIFA could make billions from the World Cup. Texas host cities will get little in return.

0

April 30, 2026

Texas court weighs whether smokable hemp can stay on shelves after Friday

0

April 29, 2026

Commentary: How a man named Connie forged a global chain that started in Texas

0

April 21, 2026

Texas restaurant owners sounding alarm over immigrant labor shortages

0

April 20, 2026

The Onion says it’s finally acquired Alex Jones’ Austin-based InfoWars

0

April 15, 2026

Old soccer fee sets Spurs at odds with San Antonio Mayor Gina Ortiz-Jones

0

April 13, 2026

How the war in Iran could affect food costs in Texas

0

April 10, 2026

Judge blocks new state rules that ban sale of smokable hemp

0

April 9, 2026

Texas is giving data centers more than $1 billion in tax breaks each year

0

April 8, 2026

Texas hemp companies sue over smokable cannabis ban and higher fees

0

April 8, 2026

A year after ‘Liberation Day,’ Trump’s tariffs are taking a toll on small businesses in Texas and nationwide

0

March 31, 2026

Texas’ ban of smokable hemp takes effect, leaving out-of-state sales in legal gray area

0

March 30, 2026

Stores scramble to sell smokeable hemp products before Texas-wide ban takes effect

0

March 25, 2026

Hey, Texas, how do you afford to live in your city? We want to hear from you

0

March 27, 2026

How Elon Musk plans to make all of the microchips his companies need

0

March 12, 2026

New South Texas refinery could bring jobs — and environmental risks

0

March 11, 2026

Texas ban on selling smokable cannabis takes effect March 31

0

March 6, 2026

A look at Elon Musk’s vast web of Texas interests

0

February 26, 2026

Meta strikes AI chip deal with AMD

0

February 20, 2026

Supreme Court strikes down Trump’s tariffs

0

February 16, 2026

Houston’s World Cup host committee commits to $15 minimum wage, human trafficking mitigation in new report

0

February 5, 2026

Construction site ICE raids hurting economy and building industry

0

January 9, 2026

Signing your kid up for soccer? You might need a second job

0

December 19, 2025

SpaceX expected to go public, launch giant IPO in 2026

0

December 18, 2025

Federal THC ban presents steep challenges to Texas hemp industry

0

December 10, 2025

The economic impact of selling plasma

0

December 4, 2025

Texas becomes the first state to invest in crypto

0

November 19, 2025

Trump is scrapping tariffs on some items. Here’s how it might impact grocery store prices

0

November 13, 2025

Deal to reopen the government includes ban that could hit Texas’ hemp industry

0

November 6, 2025

How could ‘Amazonification’ change what customers see on Whole Foods shelves?

0

November 6, 2025

US Supreme Court hears arguments in case against Trump’s tariffs

0

November 5, 2025

El Paso drive helps families, grocers weather SNAP shutdown

0

October 24, 2025

Businesses that depend on the Port of Houston are threatened by Trump’s tariffs and the government shutdown

0

October 23, 2025

Economic reality could stall President Trump’s idea to import beef from Argentina

0

October 23, 2025

Warning sign? 1.7 million vehicles were repossessed last year

0

October 14, 2025

Is the craft brewery bubble popping in Texas?

0

October 10, 2025

42-day Houston hotel strike slated to end Sunday. It’s an unprecedented labor action — in more ways than one

0

October 9, 2025

Why everyone wants to fix H-1B visas

0

October 8, 2025

The Texas Stock Exchange got federal approval. What does it mean for Dallas?

0

October 2, 2025

The longer the shutdown lasts, the greater the risk of cargo backups at Texas ports

0

October 1, 2025

Business is booming for the Beaver – but why?

0

September 30, 2025

A second man has died after Dallas ICE facility shooting, family says

0

September 24, 2025

‘It’s a way to shoot yourself in the foot’: Why H-1B visa changes could disrupt Texas’ economy

0

September 23, 2025

Many Texas retailers can no longer sell THC to customers under 21

0

September 22, 2025

Independent bookstores are having a boom. Texas is leading the charge.

0

September 18, 2025

Mortgage rates are at their lowest in nearly a year. Here’s how that impacts the housing market.

0

September 8, 2025

When will beef prices drop? We asked a rancher, a butcher and an economist

0

September 3, 2025

Time is running out on federal clean energy tax credits

0

September 2, 2025

The golden handcuffs: Why Americans aren’t moving around as much anymore

0

August 21, 2025

The credit card hangover: Consumers are sobering up from pandemic spending binge

0

August 14, 2025

$1,000-a-month pilot in Texas and Illinois shows mixed results for low-income families

0

August 8, 2025

Project Marvel: Spurs arena, Alamodome upgrades and a potential tax increase in Bexar County

0

August 8, 2025

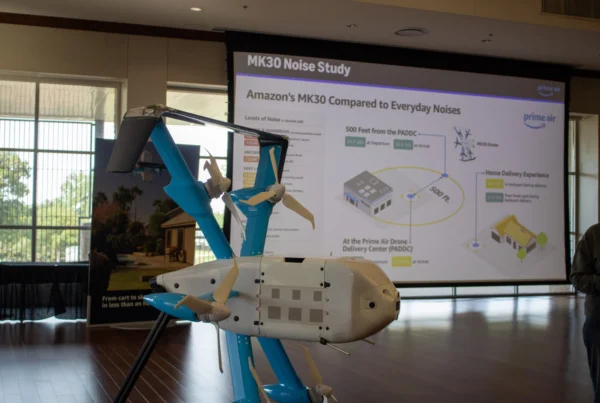

Amazon showcases new delivery drone ahead of Waco launch

0

August 6, 2025

Recent college grads have new competition for jobs: artificial intelligence

0

August 5, 2025

Texas emerges as a hub for professional services jobs

0

August 4, 2025

The growing mobile gambling industry is built on debt. Is there a fix?

0

July 28, 2025

Tariff threat hangs over Texas-Mexico economies

0

July 23, 2025

Lights or groceries?: Rising energy bills bring hard choices for low-income Texans

0

July 22, 2025

As Texans start to rebuild after the floods, many face the reality of being uninsured

0

July 22, 2025

Remote work rates stabilize in US and Texas, especially among educated workers and parents

0

July 15, 2025

How job losses across the border can affect the US

0

July 14, 2025

U.S. Rep. Henry Cuellar makes appeal for tomato industry

0

July 2, 2025

Texans could face higher costs, fewer services under Trump’s ‘big, beautiful bill’

0

July 1, 2025

Behind the tariffs: How a Texas farrier is balancing cost and craft

0

June 30, 2025

U.S. ginseng growers and animal breeders rely on exports to China. Now they wait on a trade deal

0

June 27, 2025

Underwater mortgages rise in these Texas cities as pandemic housing frenzy cools

0

June 25, 2025

Families along border cross into Mexico to save money on groceries

0

June 24, 2025

ICE raids push farm workers to stay home ‘out of fear.’ That could hurt U.S. food production

0

June 10, 2025

Americans are increasingly using buy now, pay later loans for essentials like groceries

0

June 6, 2025

A tomato tax looms for Mexican growers — and will affect U.S. consumers

0

June 5, 2025

Farmers are taking on more debt. Some worry more financial stress could be ahead

0

June 2, 2025

From promise to pullback: Texas’ tech sector faces hiring declines

0

May 29, 2025

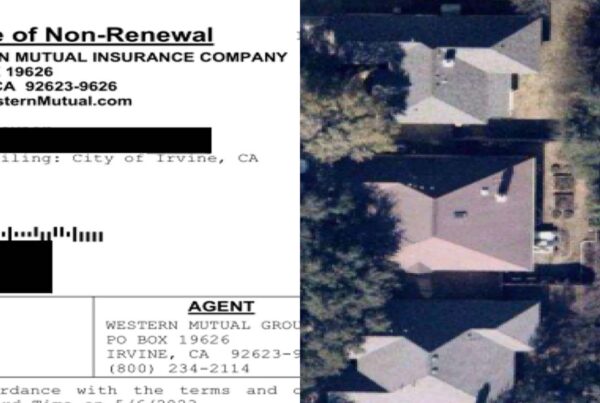

In Texas, insurers are watching your home from above. It could cost you coverage.

0

May 28, 2025

A thirsty Tesla refinery could exacerbate Corpus Christi’s water crisis

0

May 23, 2025

The real price of joining free loyalty programs to get discounts at checkout? Your data privacy.

0

May 16, 2025

Kroger found to be overcharging customers on sale items, resulting in dent to customers’ wallets

0

May 7, 2025

Houston team finds many cases of shrimp fraud among Gulf Coast restaurants

0

May 6, 2025

How in-house brands have taken over shoppers’ grocery carts

0

April 30, 2025

‘People are worried’: Current consumer spending trends highlight concerns over the economy

0

April 29, 2025

100 days, two Americas: Assessing the impact of President Trump’s policies on California and Texas

0

April 28, 2025

‘You’re gonna be begging for a two- to four-hour wait time pretty soon’ local social security union president warns

0

April 24, 2025

From pints to playgrounds: Texas breweries reinvent themselves to stay afloat

0

April 22, 2025

Here’s how China’s tariffs could impact the Texas economy

0

April 18, 2025

Is it a good time to buy a car? Likely not, experts say.

0

April 17, 2025

Does one company’s rising Amazon prices hint at what tariffs could bring?

0

April 11, 2025

A federal employee cut at National Marine Sanctuary is throwing part of its mission ‘into disarray’

0

April 11, 2025

Dallas may soon have three stock exchanges. What does that mean for the Texas economy?

0

Next Entries »

NO MATTER WHERE YOU ARE,

YOU’RE ON TEXAS STANDARD TIME